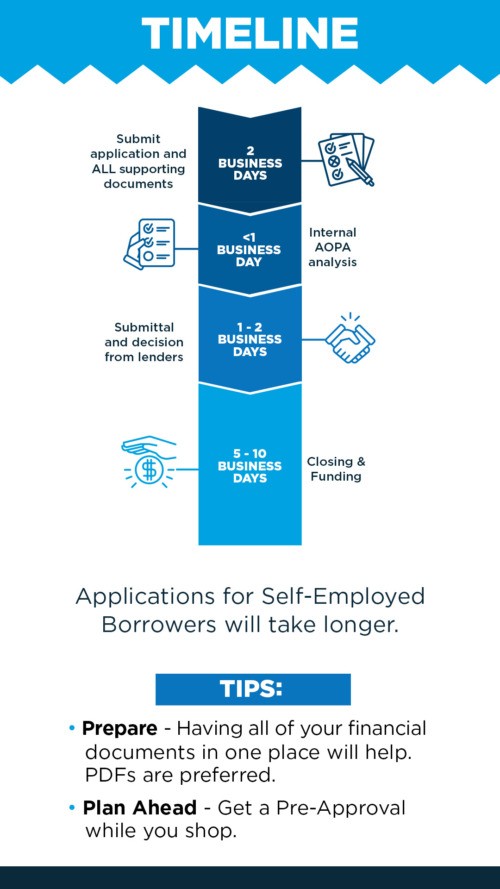

Aircraft Financing Explained

5 min read

We all dream about slick personal aircraft — firing up the engines on our own jet, or hovering above traffic in a turbine chopper. The high-flying dreams might live in our heads, but we suspect that the majority of our bank accounts leave something to be desired.

How do you afford a plane or helicopter without winning the lottery? It is simple, aircraft financing.

Finding the appropriate loan or lease can turn ownership into a reality.

In this guide, I'm going to tell you everything (yes, everything) you need to know about aircraft financing and how it can help bring your dreams of flying to life. Let's do this!

Different Types of Aircraft Loans and Leases

If cash in the bank is not desirable, well, you have plenty of other choices available to you for paying for an aircraft. These are some of the financing setups common among pilots:

Secured Loans Similar to a home mortgage, secured loans are demand loans that collateralize the aircraft thereby reducing the risk exposure of a lender. These are offered by banks, credit unions, and specialized finance firms.

Pros

- Rates lower than unsecured loans

- Predictable fixed monthly payments for budgeting

Cons

- Big down payment needed, typically 20-30% minimum

- Losing ability to take aircraft away from you for missed payments

Operating Leases An operating lease allows you to make the monthly payments for flying an aircraft without physically owning it. It's like a long-term rental.

Pros

- Set foot for less or nothing capital

- No ownership of asset = zero risk of losing aircraft

Cons

- Over time the sum of leasing costs surpasses loan costs

- During which aircraft usage and any modifications to it are subject to strict limits

Unsecured Loans

These are loans that are not collateralized with the aircraft. However, their rates are higher and the repayment terms also shorter than those of secured financing.

Pros

- Keep 100% of the ownership and control of planes

- Shortest loan terms, repayment choices

Cons

- Interest rates that are the highest in a long while

- For this reason, large balloon payments were commonly required

Partnership Share Loans Finance is part of the co-owned airplane to reduce your total amount to be borrowed.

Pros

- Lower buy-in and operating costs

- Shared expenses with partners

Cons

- Complex legal and scheduling logistics

- Compromises on usage, modifications

What Types of Airplanes Can you Get Financed?

That includes anything from small pistons to corporate jets, and just about every new and used personal aircraft in between:

- Single engine piston aircraft (Cessna 172s, Piper Cherokees, etc.)

- Turboprops, multiple engines (Beechcraft King Airs Pilatus PC-12s et al.)

- Light to midsize business jets (e.g. Cirrus VisionJet, Embraer Phenom 100)

- Piston helicopters (R44s, 206s, etc.):

- Turbine up tykes (Bell 429s, Airbus H125s, etc.)

- Certain kitplanes and experimental classes of homebuilt aircraft

Factors such as the make, model, age, condition, and maintenance history of an aircraft influence its value in the eyes of a lender when they determine financing terms. Financing for rare or older plane types may be limited

Can You Qualify for an Aircraft Loan?

Aircraft are much pricier than cars or boats, and so standards for getting financing approved are tougher:

- Excellent credit score - 680+ minimum, 720+ ideal

- Proof of substantial net worth and liquid assets

- Stable income source that reliably covers payments

- Aviation experience - pilot's license, 200+ hours ideal

- Solid business finances if using for charter

If you have loans and bank accounts that are under the same lender, it would bend the approval odds on your side a bit.

The key is that you have to build up your qualifications before applying.

Typical Aircraft Loan Terms and Rates

Although you can sprinkle in the fine details of each loan, here are some average aircraft financing terms:

- Down payment - 20-40% of aircraft purchase price

- Loan amount - $200k+ for light aircraft, millions for business jets

- Loan term - 10-20 years generally

- Interest rates - 4-6% for well qualified buyers, higher for riskier applicants

Typically, lenders will have more favorable terms for new aircraft as opposed to a used model. How long till you sign the contract of a lifetime?!

Tip: A shorter term (10 years) gives a lower total interest paid, but you could always pay it off early.

How to Pick the Best Aircraft Lender

If you have been pre-approved ensure to look for financing Here are some of the best national lenders:

Banks

Specialized Lenders

- Global Jet Capital

- LCI Aviation / Sikorsky Financial

- Piper Aircraft Finance

- Textron Aviation Finance

It makes pre-approval faster, if you have built up a relationship with the providers for long. Which enables you to pull the trigger when the right plane comes along.

Consider more than interest rates — which lender aligns best with your timeline, experience level, budget flexibility, and intended use of the aircraft? Helping us, you know, search for the best match.

Expert Tips for Getting Aircraft Financing

Now, here are my best tips:

- You should research lenders and the different options that are out there 1-2 years in advance of your purchase. Hasty financing results in increased rates, or denial.

- Pre-qualify to catch any problems early. Ensure that you have met every requirements of credit, income, and asset. This makes it easier in later stages when we have to follow the formal application process.

- Shop around for rates and terms with different lenders. More choices mean improved negotiating leverage. However, keep loan shopping to a short period to minimize dings on your credit.

- Take along a co-signer for additional security. This can be useful if you are a new pilot, or have little credit history.

- Do yourself a favor and cookie-cutter your aviation experience, assets and stability to strengthen your appeal. This neutralizes potential lenders' risk.

- Maintain your logbooks and records for your aircraft Complete maintenance records and ownership documents increase the resale value of your plane. Which helps you when you upgrade in the future.

Time to Buy Your Wings!

And there you have it: everything you need to know about financing other than how to fully realize your aviation dreams. It's not simply about getting the best available interest rate. The right homework, planning and lending partner are everything.